pm-youth-loan-scheme

Starting or expanding a business in Pakistan requires more than just a brilliant idea; it demands accessible, low-cost capital. For young entrepreneurs and small-scale farmers struggling to secure funding through traditional corporate banking channels, the Prime Minister’s Youth Business & Agriculture Loan Scheme (PMYB&ALS) provides a direct lifeline.

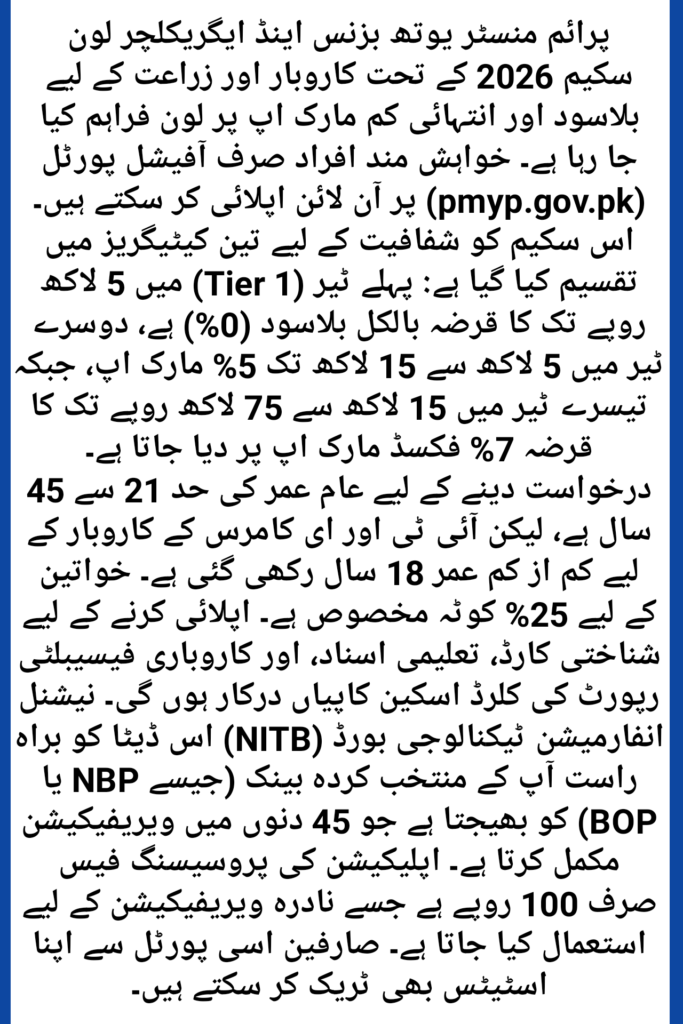

Through this centralized initiative, the government aims to reduce unemployment and stimulate economic growth by providing highly subsidized, low-interest commercial loans. If you are ready to turn your entrepreneurial vision into reality, accessing the official PM Youth Loan Scheme 2026 online application link is your crucial first step toward securing up to PKR 7.5 million in capital.

The Structural Core of the PM Youth Loan Scheme 2026

The PM Youth Loan Scheme functions through a streamlined digital framework designed to maximize transparency and minimize bureaucratic delays. Rather than managing physical paper stacks, the entire intake pipeline is hosted securely on the national web framework.

The Official Online Application Link and Hosting Portal

The sole authorized portal for filling out and submitting your financing request is the official Prime Minister’s Youth Programme website. You can access the application portal directly at pmyp.gov.pk.

The digital processing engine behind this setup is built and optimized by the National Information Technology Board (NITB) under the Ministry of Information Technology and Telecommunication. This central infrastructure instantly routes your submitted data straight to the credit review desk of your chosen commercial bank.

[ APPLICANT ] ──► [ pmyp.gov.pk Portal ] ──► [ NITB Routing Engine ] ──► [ Chosen Executing Bank ]

Navigating the Dynamic Tier and Interest Rate Matrix

To ensure equal opportunity for both micro-startups and scaling enterprises, the PMYB&ALS segments its funding into three distinct operational tiers, each carrying unique mark-up profiles:

- Tier 1 (T1) — Up to PKR 500,000: This tier is completely mark-up free (0% interest). It is designed for micro-enterprises and small retail setups. These loans are completely clean, requiring only the personal guarantee of the borrower.

- Tier 2 (T2) — PKR 500,001 to PKR 1.5 Million: Carries a highly subsidized, fixed interest rate of 5% per annum. Like Tier 1, this tier operates as a clean facility, meaning you do not need to pledge heavy commercial property to qualify.

- Tier 3 (T3) — PKR 1,500,001 to PKR 7.5 Million: Tailored for manufacturing units or sizable agricultural transformations, this tier carries a fixed mark-up rate of 7% per annum. Security requirements for Tier 3 follow the individual credit policies of the executing bank.

PM Youth Loan Scheme Clear Eligibility Benchmarks & Document Checklist

The government has established clear eligibility parameters to protect public funds while maintaining broad accessibility for young citizens.

Who is Eligible to Apply for the 2026 Phase?

The entry requirements focus strictly on age, business potential, and basic qualifications for specialized fields:

- Standard Age Bracket: All Pakistani citizens holding a valid CNIC aged between 21 and 45 years possess the baseline eligibility to apply as sole proprietors.

- The IT & E-Commerce Exception: To foster digital freelance growth, the lower age limit drops to 18 years for technology-focused businesses, provided the applicant holds at least a Matriculation or equivalent certificate.

- Corporate & Partnership Extensions: For joint ventures or private limited setups, only one of the core directors or partners needs to fall within the mandatory age bracket.

- The Gender Quota: To foster financial inclusion, 25% of the total loan allocations are strictly reserved for female entrepreneurs across Pakistan.

Mandatory Verification Documents Checklist

Before opening the online application link, compile scanned, legible versions of these documents to prevent automated portal rejections:

- A clear, front-and-back digital color scan of your valid CNIC/SNIC.

- Your highest educational degrees, vocational certificates, or verified technical diplomas.

- Proof of entrepreneurial experience or specific trade expertise (where applicable).

- A concise, clear business feasibility write-up including realistic projected revenue and operation costs.

- Two distinct character references with their accompanying CNIC numbers and active phone contacts.

- Your Consumer Number for the electricity connection at your primary residential address.

PM Youth Loan Scheme Online Application and Tracking Process

Completing the form requires focused attention. The system does not allow massive structural edits once the processing fee is logged, so accuracy from the start is paramount.

1.Initialize Registration via PMYP:Step 1.

Visit pmyp.gov.pk and select the “Youth Business & Agriculture Loan Scheme” tab to open the new applicant wizard.

2.Input Core Identity Details:Step 2.

Enter your CNIC number and its precise date of issuance. The portal connects directly with the NADRA verification API to instantly authenticate your structural identity data.

3.Select Your Executing Bank:Step 3.

Choose your preferred commercial bank from the listed executing partners (e.g., National Bank of Pakistan, Bank of Punjab, Askari Bank, or Allied Bank). This choice dictates who will review your credit history.

4.Fill Out the Comprehensive Application Form:Step 4.

Complete all 9 structural fields of the form, including personal details, business info, asset structures, and feasibility estimations. You can switch the form view between English and Urdu on the fly.

5.Pay Processing Fee and Submit:Step 5.

Review your data and click submit. The portal requires a nominal, one-time, non-refundable form processing fee of PKR 100, which includes the mandatory NADRA verification toll.

Pro Tip: Once submitted, use the same portal to track your application status. Your application will shift through transparent stages: from Submitted to Scrutiny, Under Process, and finally Approved or Regretted.

PM Youth Loan Scheme Loan Tenors, Equity Ratios, and Collateral

Before signing your facility offer letter, you must understand the long-term repayment mechanics and financial responsibilities involved.

Repayment Terms and Grace Periods

The PM Youth Loan Scheme features generous repayment durations designed to give new businesses ample time to find their footing:

- Long-Term/Development Loans: Tiers 2 and 3 offer an extended loan tenor of up to 8 years, which includes a valuable 1-year grace period where you only pay the mark-up amount rather than the full principal.

- Working Capital/Production Financing: Designed for inventory procurement or crop cycles, these loans carry a maximum tenor of 5 years.

- Agricultural Production Loans: These are tied directly to crop cycles, featuring a maximum 1-year tenor with a single lump-sum repayment due immediately upon harvest.

Debt-to-Equity Ratio Matrix

If you are launching a completely brand-new startup, you must contribute a small percentage of equity to demonstrate commitment:

| Business Status | Tier 1 Equity Ratio | Tier 2 Equity Ratio | Tier 3 Equity Ratio |

| New Business Launch | 90:10 (10% Applicant Equity) | 90:10 (10% Applicant Equity) | 80:20 (20% Applicant Equity) |

| Existing Business Expansion | Nil (0% Equity Required) | Nil (0% Equity Required) | Nil (0% Equity Required) |

Your equity contribution can be provided in the form of raw cash deposits or recognized immovable property evaluations after your loan receives formal bank approval.

Frequently Asked Questions

What is the exact online application link for the PM Youth Loan Scheme in 2026?

The official, centralized link to apply for the scheme is pmyp.gov.pk . Do not submit your CNIC details or personal credentials on external websites, blogs, or unverified social media links.

Are there any hidden processing charges or early settlement fees?

No. Aside from the initial PKR 100 NADRA verification fee paid during submission, there are zero processing fees. Furthermore, the State Bank of Pakistan mandates a 0% early settlement charge policy for this scheme, meaning you can pay off your entire outstanding loan early without penalties.

Can I apply for two different business loans under this scheme?

Yes, but within a strict boundary. A single borrower can avail a maximum of two concurrent loans (typically one long-term development loan and one short-term working capital loan), provided the combined total of both loans does not exceed the overall Tier 3 limit of PKR 7.5 million.

How long does it take for the bank to process and disburse the loan?

The State Bank of Pakistan has instructed executing banks to complete the entire processing cycle—from initial online routing to final credit approval—within a target window of 45 working days, provided all submitted documentation is verified and clean.

The Strategic Path Forward for Your Venture

The PM Youth Loan Scheme 2026 provides an unprecedented opportunity to secure low-cost capital without navigating the typical hurdles of corporate lending. However, receiving approval requires treating the online portal with the care of a professional corporate presentation. Take the time to build a realistic business feasibility model, ensure your credit history is pristine, and use the official link at pmyp.gov.pk to launch your application. By matching a subsidized public loan with a solid execution plan, you can successfully build a sustainable, scalable business.